For wealth advisors, family offices and private client teams, relocation planning used to start with a simple question:

Where should the client move?

For many clients, that question is now too narrow.

In other words, many wealthy families are already multi-jurisdictional before any formal relocation plan begins.

Their residence, business activity, asset location, family needs and future optionality may already sit across several legal systems.

The advisory question is not only where they should move next. It is whether their existing footprint is resilient, concentrated or exposed to policy change.

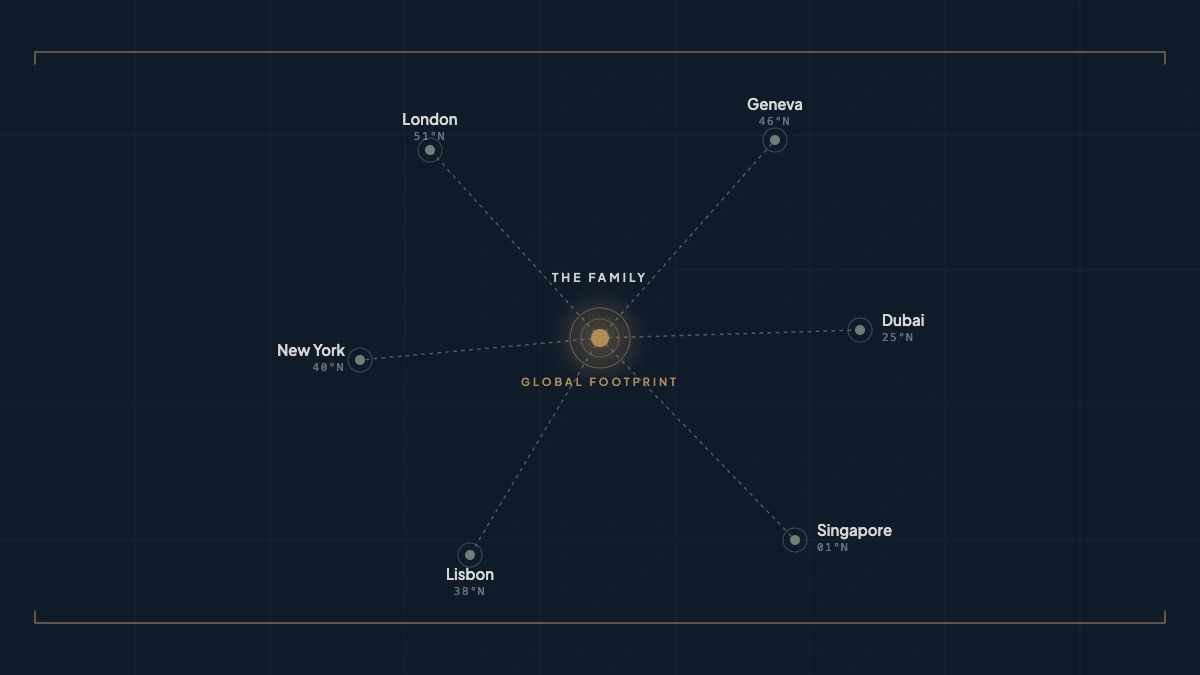

That is the logic of the sovereign portfolio.

A sovereign portfolio is a structured view of a client's exposure across jurisdictions: where they live, where their company is managed, where assets are held, where family needs are anchored and where future optionality exists.

It is not complexity for its own sake.

It is a way to model jurisdictional risk.

Policy Volatility Creates Jurisdictional Concentration Risk

A client can be diversified across asset classes, currencies and managers while remaining highly concentrated in one jurisdiction for residence, tax, business management or family planning.

That concentration matters because policy can change quickly.

Spain ended its golden visa route for real estate investors in April 2025 after years of debate around foreign investment and housing affordability. The UK replaced its long-standing non-dom remittance-basis regime from April 2025, changing planning assumptions for internationally wealthy residents who had relied on it for years. Italy raised its annual flat tax on foreign income for new residents in successive steps — from €100,000 to €200,000 in 2024, and then to €300,000 from January 2026 — showing that even regimes designed to attract wealthy newcomers can be recalibrated.

None of these examples means those countries are unattractive.

Spain remains a desirable lifestyle jurisdiction. The UK remains a major financial, legal and educational center. Italy remains compelling for many families and entrepreneurs.

The point is that rules change.

A relocation plan, tax strategy or residence pathway that looks attractive at the point of entry may need to be reassessed later. For advisors, the question is not whether policy risk can be eliminated. It cannot.

The question is whether the client's footprint can absorb change.

What Is a Sovereign Portfolio?

A sovereign portfolio is not an offshore tax strategy. It is not a promise of political immunity. It is not a recommendation that every client should spread their life across as many jurisdictions as possible.

It is a planning framework for understanding exposure.

A useful sovereign portfolio usually has four layers:

| Layer | Core question | Why it matters |

|---|---|---|

| Residence layer | Where does the client live, and where are they tax resident? | Drives personal tax, immigration status, lifestyle, healthcare, education and day-count exposure |

| Business layer | Where is the company incorporated, managed and operated? | Creates corporate tax, permanent establishment, management/control and substance considerations |

| Asset layer | Where are financial and physical assets held? | Affects custody, reporting, succession, banking, real estate and tax treatment |

| Optionality layer | What alternatives exist if the primary jurisdiction becomes less attractive? | Supports backup residence, citizenship planning, relocation feasibility and long-term resilience |

This framework helps advisors see where advice streams intersect.

A client may describe the decision as "moving to Portugal" or "setting up in Dubai" or "relocating to Italy." But the real footprint may involve family members in several countries, a company managed elsewhere, assets held across multiple markets and a citizenship plan that depends on residence continuity.

The sovereign portfolio makes that exposure visible.

It also shows where diversification helps, and where it creates friction.

A founder may choose one country as a family lifestyle base, another as a company operating hub and another as a banking or asset custody jurisdiction. That may create resilience, but only if the layers work together.

The residence decision must be understood alongside business management. The company structure must be reviewed alongside the founder's working pattern. The asset layer must be assessed alongside reporting, succession and tax-residence implications.

The goal is not to create separation for its own sake.

The goal is to avoid accidental concentration.

The Compliance Friction Layer: CFC, PE and Economic Substance

A multi-jurisdictional footprint can create resilience, but it also creates compliance friction.

Multiple jurisdictions mean multiple rulebooks. Those rulebooks may overlap, conflict or interpret the same facts differently. A client may believe their personal life and business structure are separate. A tax authority may focus on where decisions are actually made.

Three risk areas should be surfaced early in any serious cross-border planning discussion.

Controlled Foreign Corporation Risk

Controlled foreign corporation rules can become relevant when a client is tax resident in one country while controlling a company in another.

For founders, business owners and family investment companies, this matters when personal residence and corporate location diverge.

The key question is not only where the company is incorporated.

It is whether the client's residence country can attribute company income, profits or retained earnings back to them under local CFC or anti-avoidance rules.

That question requires specialist tax advice. But it should be flagged before the client commits to a relocation decision, not after.

Permanent Establishment and Management Control

Permanent establishment risk arises when a business creates enough presence or activity in a country for that country to claim taxing rights over part of the business.

For globally mobile founders, this can happen unintentionally.

A client may relocate for lifestyle reasons while continuing to negotiate contracts, direct employees, approve strategy, manage key clients or make board-level decisions from their new country of residence.

Even if the company remains incorporated elsewhere, tax authorities may look at where effective management is taking place.

That makes the client's working pattern part of the relocation analysis.

Where are key decisions made? Where are directors based? Where are contracts negotiated? Where is IP developed or controlled? Where are senior employees located?

A relocation decision that ignores those questions can create corporate tax exposure the client did not intend.

Economic Substance

Economic substance is the practical test behind many cross-border structures.

A company may be legally established in one jurisdiction, but advisors still need to consider whether it has the people, governance, premises, decision-making and operational activity to support that position.

This does not mean every client needs a large local office or complex infrastructure.

It does mean that paper arrangements are increasingly fragile.

For advisors, the point is to identify where substance questions are likely to arise, what assumptions need testing, and where legal or tax specialists should be brought in before the client relies on the structure.

What This Means for Wealth Advisors

The sovereign portfolio is useful because it changes the advisory conversation.

Instead of asking only which country is most attractive, advisors can ask how each country interacts with the client's wider footprint.

- Will personal residence create CFC exposure?

- Could the client's working pattern create permanent establishment risk?

- Does the company have enough substance in its operating jurisdiction?

- Are assets held in jurisdictions that remain suitable after the move?

- Could the destination create wealth tax, exit tax, inheritance tax or reporting issues?

- Does the client have credible optionality if the primary jurisdiction changes direction?

These are not questions a static country guide can answer properly.

They require a structured comparison of jurisdictions, client priorities and risk areas.

For advisors, the value is not in automating complex structuring. It is in identifying the questions that need to be asked before decisions harden.

Neoria helps advisors compare jurisdictions across residency, tax, business, cost of living, lifestyle and long-term suitability factors. It supports early-stage analysis by making trade-offs, assumptions and risk areas easier to explain before specialist tax, legal or immigration advice begins.

The client may still need bespoke advice.

But the advisor can enter that conversation with a clearer view of the client's options, exposures and next questions.

The Strategic Question Has Changed

The modern global family is not simply mobile.

It is distributed.

Family, assets, business operations, tax exposure and future plans often sit across multiple jurisdictions at the same time.

That changes the planning question.

It is no longer only:

Where should this client move?

It is:

How exposed is this client to each jurisdiction, and what happens if one of those jurisdictions changes the rules?

That is the logic of the sovereign portfolio.

For clients, it creates better visibility.

For advisors, it creates a more strategic conversation.

And in a world where tax, residence, immigration and political risk can change quickly, that conversation is becoming essential.

Related resources

What Is Jurisdictional Risk? A Practical Guide for Wealth Advisors

A practical framework for identifying jurisdictional exposure across residence, assets, business and family planning.

Europe's Immigration Rules Are Becoming Less Predictable

Why advisors need to model pathway risk across residence, permanent residence and citizenship outcomes.

Cross-Border Relocation Advisory Software: How Wealth Advisors Can Scale Client Conversations

How advisor-led software helps structure, qualify and scale relocation conversations.

FAQ: Sovereign Portfolios and Jurisdictional Risk

What is a sovereign portfolio?

A sovereign portfolio is a structured view of a client's exposure across jurisdictions, including residence, business operations, asset location, family needs, tax position and future optionality. It helps advisors understand whether a client's global footprint is resilient, concentrated or exposed to policy change.

Is a sovereign portfolio the same as offshore tax planning?

No. A sovereign portfolio is not about avoiding rules. It is about understanding how a client's life, business and assets interact with different legal, tax and immigration systems. Any tax, legal or investment implications should be reviewed by qualified specialists.

Why does jurisdictional risk matter for wealth advisors?

Jurisdictional risk matters because tax rules, residence regimes, visa pathways, wealth taxes, reporting obligations and political priorities can change. If a client's personal life, company, assets and family plans are concentrated in one jurisdiction, a policy change can affect the whole structure.

What are the main risks in a multi-jurisdictional footprint?

Common risks include controlled foreign corporation exposure, permanent establishment risk, management and control issues, economic substance requirements, tax residency conflicts, reporting obligations, exit taxes, wealth taxes and succession complications.

Does every client need a multi-jurisdictional strategy?

No. For many clients, a simpler single-country move may be more suitable. A sovereign portfolio framework is most useful for clients who already have cross-border family, business or asset exposure, or who need to understand how a relocation decision affects their wider footprint.

How can advisors use Neoria in sovereign portfolio planning?

Neoria helps advisors compare jurisdictions across residency, tax, business, cost of living, lifestyle and long-term suitability factors. It supports early-stage analysis by identifying trade-offs and risk areas that may require further specialist review.